In today’s complex financial landscape, insurance stands out as a critical component of personal and business risk management, promising peace of mind in the face of unforeseen events. Whether it’s safeguarding one’s health, property, vehicle, or livelihood, insurance policies play a pivotal role in securing financial stability.

However, this system, built on trust and the principle of mutual benefit, faces a formidable adversary: insurance fraud.

Insurance fraud is an illicit activity that undermines the very foundations of the insurance sector, turning safety nets into opportunities for deception. This malpractice is not confined to one area but permeates various forms of insurance, from automotive to health, homeowners, and workers’ compensation.

It involves deliberate acts of falsification, exaggeration, or outright lies told to insurance companies with the intent of gaining financial benefits that would otherwise be unobtainable. The consequences of such actions are far-reaching, affecting not only the perpetrators and the insurance companies but also the vast majority of policyholders who adhere to the rules.

The Nature of Insurance Fraud

Insurance fraud is a multifaceted issue that manifests in numerous ways, each carrying its own set of challenges and implications for the industry and consumers alike. At its core, insurance fraud is characterized by the intentional deception of insurance companies for financial gain.

This deception can range from slight exaggerations to outright lies and encompasses a wide spectrum of activities across different types of insurance.

The Act of Deception

The act of deception in insurance fraud encompasses a deliberate manipulation or distortion of facts aimed at illicitly gaining financial benefits from an insurance policy. This fraudulent behavior is not only a breach of trust but also a significant legal offense that can lead to severe repercussions for individuals involved.

Understanding the mechanisms, motivations, and consequences of such acts sheds light on the complexity of insurance fraud and underscores the importance of vigilance and integrity within the insurance system.

Mechanisms of Deceit

Insurance fraud through deception can manifest in various forms, each tailored to exploit vulnerabilities within the insurance process. These mechanisms include:

- Fabrication: Creating a completely false claim or event, such as a theft that never occurred or an injury that was never sustained.

- Exaggeration: Inflating the value of a claim, such as reporting higher costs for repairs or medical treatments than were actually incurred.

- Misrepresentation: Providing false information on an insurance application to obtain a policy under false pretenses or at a reduced rate, such as lying about one’s health condition or the actual use of a property.

- Omission: Failing to disclose relevant information deliberately, which if known, would affect the coverage terms or premium costs, such as not reporting a pre-existing condition or previous damage to a property.

Motivations Behind Fraudulent Acts

The motivations driving individuals to commit insurance fraud are varied, but they often revolve around financial gain or alleviating financial strain. For some, the temptation of receiving a payout without the corresponding legitimate claim can be compelling.

Others may justify their actions by perceiving insurance companies as large, impersonal entities from which they are reclaiming what is rightfully theirs or compensating for perceived overpayments in premiums.

Economic pressures, such as unemployment, debt, or the desire for financial improvement, also play a significant role. In these cases, insurance fraud is rationalized as a means to an end, a temporary solution to a pressing financial problem.

Types of Insurance Fraud

Insurance fraud is a pervasive issue that spans across various types of insurance, each with its own set of tactics and consequences. Understanding these categories is essential for recognizing the signs of fraud and implementing effective prevention strategies.

Automotive Insurance Fraud

Automotive insurance fraud is one of the most common forms of insurance fraud, encompassing a range of deceptive practices related to vehicle damage, theft, and accidents.

- Staged Accidents: Fraudsters deliberately cause accidents to file claims against innocent motorists or their own policies. These can involve multiple vehicles and fake witnesses to create a plausible scenario for injuries or damage.

- Exaggerated Claims: After a legitimate accident, individuals may inflate the extent of the damage or claim for pre-existing damage, seeking compensation well beyond the actual repair costs.

- Vehicle Theft Fraud: Owners may report their vehicle stolen to claim the insurance payout, when in reality, the vehicle is hidden or sold.

- Phantom Victims: Claims include individuals who were not actually involved in the accident, artificially inflating the payout for medical treatments or personal injuries.

Health Insurance Fraud

Social media is an invaluable tool for crisis communication, allowing for rapid dissemination of information during emergencies. Effective use of these platforms can enhance public safety and trust, particularly when accurate, timely information is shared during critical incidents.

For instance, during natural disasters or active shooter situations, law enforcement agencies can provide real-time updates, safety instructions, and reassurance to the public, demonstrating their role as protectors and information providers.

Challenges and Considerations

Health insurance fraud can be particularly damaging, affecting both private insurers and government-funded programs.

- Provider Fraud: Medical providers may bill for services not rendered, overcharge for services provided, or perform unnecessary procedures to increase billing. This includes falsifying a patient’s diagnosis to justify certain tests or surgeries.

- Member Fraud: Individuals commit fraud by allowing someone else to use their insurance, submitting claims for non-prescribed drugs, or fabricating injuries or illnesses to receive prescription medication or medical services.

Homeowners Insurance Fraud

Fraud within homeowners insurance often involves claims related to property damage or loss.

- Inflated or Fake Claims: Policyholders may exaggerate the extent of damage from an event, such as a storm or burglary, or fabricate a loss entirely.

- Intentional Damage: Some homeowners intentionally cause damage to their property to file a claim, including setting fire to their home (arson) under the guise of an accident.

- False Burglary Reports: Claiming for high-value items that were allegedly stolen during a burglary, when in fact, no burglary occurred or the items were never owned.

Workers’ Compensation Fraud

Workers’ compensation fraud is detrimental to businesses and employees, undermining the system designed to protect workers injured on the job.

- Fake Injuries: Employees claim to have suffered a workplace injury that never occurred or exaggerate the severity of a minor injury to receive benefits.

- Misreported Wages or Misclassification: Employers commit fraud to reduce insurance premiums by underreporting payroll, misclassifying workers as independent contractors, or falsifying job descriptions to qualify for lower rates.

- Return to Work Fraud: Employees receiving benefits due to a workplace injury may return to work (often “under the table”) while continuing to claim they are unable to work because of the injury.

The Challenges of Detecting and Combating Insurance Fraud

Detecting and combating insurance fraud presents a complex set of challenges that insurance companies, regulators, and law enforcement agencies must navigate. These challenges stem from the evolving nature of fraudulent schemes, the sophistication of fraudsters, and the intrinsic limitations of prevention and detection systems.

Understanding these obstacles is crucial for developing more effective strategies to mitigate the impact of insurance fraud on the industry and consumers alike.

Evolving Nature of Fraudulent Schemes

One of the primary challenges in fighting insurance fraud is the constant evolution of fraudulent schemes. As technology advances and the insurance industry adopts new practices, fraudsters adapt their methods to exploit new vulnerabilities.

This continuous game of cat and mouse means that strategies that were effective yesterday may not work tomorrow, requiring constant vigilance and adaptation from those tasked with detecting and preventing fraud.

Sophistication of Fraudsters

Many fraudsters employ increasingly sophisticated techniques to evade detection. This includes the use of technology to create realistic forgeries, leveraging social engineering to obtain sensitive information, and complex conspiracies involving multiple parties to orchestrate large-scale frauds.

The level of sophistication not only makes detection more difficult but also complicates the investigation and prosecution of these crimes.

Data Volume and Analysis

The sheer volume of data that must be analyzed to detect fraud poses another significant challenge. Insurance companies process thousands of claims daily, each of which must be evaluated for potential signs of fraud.

While advanced analytics and machine learning algorithms have significantly improved the ability to sift through this data, false positives remain a concern, and genuine fraud can still slip through the cracks.

Balancing the sensitivity of fraud detection systems to minimize both false positives and false negatives is a complex and ongoing challenge.

Legal and Regulatory Constraints

Legal and regulatory frameworks designed to protect consumer rights can also limit the ability of insurers to investigate potential fraud. Privacy laws, for example, may restrict access to certain types of information that could be useful in fraud detection.

Additionally, the burden of proof for prosecuting insurance fraud is high, requiring clear and convincing evidence that fraud has occurred. These constraints necessitate careful balancing between vigorous fraud prevention efforts and adherence to legal standards and consumer protections.

Resource Allocation

Effective fraud detection and prevention require significant resources, including specialized staff, advanced technology, and continuous training. Allocating these resources efficiently is a challenge, especially for smaller insurance companies that may lack the financial capacity of larger firms.

Furthermore, the cost of implementing sophisticated fraud detection systems must be weighed against the potential savings from reduced fraud, a calculation that is not always straightforward

Collaboration and Information Sharing

Combating insurance fraud effectively often requires collaboration across different entities, including insurance companies, law enforcement agencies, and regulatory bodies.

However, information sharing can be hampered by competitive concerns, data privacy regulations, and logistical obstacles. Establishing trust and mutual benefit is crucial for overcoming these barriers and enhancing collective efforts against fraud.

Consequences of Insurance Fraud

The consequences of these types of fraud are far-reaching. Beyond the immediate financial impact on insurance companies—which ultimately gets passed down to consumers in the form of higher premiums—there are broader societal implications.

Fraud erodes trust in the insurance system, increases the burden on the legal and healthcare systems, and, in some cases, endangers lives. For the perpetrators, being caught can lead to severe legal penalties, including fines, imprisonment, and a lasting criminal record that can impact future employment and social standing.

Insurance fraud has far-reaching consequences beyond the immediate financial losses. It results in increased insurance premiums for all policyholders, strains the legal and judicial systems, and can endanger lives in cases of staged accidents or arson.

Moreover, the societal impact cannot be underestimated, with fraud contributing to a general erosion of trust in the insurance system.

Financial Impact on the Insurance Industry

Insurance fraud results in billions of dollars in losses for insurers annually. These losses are not absorbed by companies alone; they are ultimately passed down to consumers in the form of higher premiums.

The need for insurers to invest in sophisticated fraud detection systems, employ specialized investigative staff, and cover the costs associated with legal proceedings further contributes to operational expenses, which, in turn, influence premium rates.

Increased Premiums for Consumers

The most direct impact of insurance fraud on consumers is the increase in insurance premiums. When insurers face financial losses due to fraudulent claims, they often have no choice but to raise premium rates to maintain their reserves at a level sufficient to cover future claims.

This means that honest policyholders bear the financial burden of fraud, paying more for their insurance coverage than they otherwise would in a fraud-free environment.

Erosion of Trust

Insurance is built on a foundation of trust between insurers and their policyholders. Fraudulent activities erode this trust, leading to a more adversarial relationship between consumers and insurers.

When insurance companies are forced to implement stricter claims review processes and adopt more rigorous investigation procedures to combat fraud, it can result in delays and additional scrutiny for legitimate claims, inconveniencing honest policyholders and potentially leading to a perception of insurers as overly skeptical or untrustworthy.

Societal and Economic Consequences

The societal impact of insurance fraud is profound. Beyond the economic implications, certain types of fraud, particularly those involving staged accidents or arson, can put human lives at risk.

Staged automobile accidents not only aim to defraud insurance companies but also endanger the lives of unsuspecting drivers and passengers.

Similarly, arson for insurance fraud purposes poses a direct threat to public safety, risking the lives of occupants, neighbors, and emergency responders.

Insurance fraud also diverts law enforcement and legal resources away from other critical areas, impacting the broader criminal justice system. The time and resources spent investigating, prosecuting, and adjudicating fraud cases could be directed toward addressing violent crimes and other pressing societal issues.

Legal and Personal Repercussions for Perpetrators

The legal and personal repercussions for individuals caught committing insurance fraud are severe and multifaceted, reflecting the seriousness with which jurisdictions around the world treat these crimes.

Insurance fraud not only undermines the financial stability of insurance companies but also affects honest policyholders through increased premiums and deteriorates the trust within the insurance system. As such, the consequences for perpetrators extend beyond legal penalties to include significant personal and professional impacts.

Legal Repercussions

- Criminal Charges: Insurance fraud is typically treated as a criminal offense, which can lead to charges ranging from misdemeanors for smaller infractions to felonies for more significant acts of fraud. The severity of the charge often depends on the amount of money involved, the method of deceit used, and whether the perpetrator has committed prior offenses.

- Imprisonment: Felony charges for insurance fraud can result in lengthy prison sentences, especially for large-scale frauds or when the fraud involves additional criminal activities such as arson, theft, or bodily harm. The prospect of serving time in prison is a stark reality for those convicted of insurance fraud.

- Fines and Restitution: In addition to or in lieu of imprisonment, courts can impose hefty fines on individuals convicted of insurance fraud. Perpetrators may also be ordered to pay restitution to the insurance company or to any victims who suffered financial losses as a result of the fraudulent activity. These financial penalties can amount to thousands or even millions of dollars, depending on the scope of the fraud.

- Probation: Individuals convicted of insurance fraud may be placed on probation for a period of time, during which they must comply with specific conditions set by the court. Violation of probation terms can result in additional penalties or imprisonment.

Personal and Professional Consequences

- Permanent Criminal Record: A conviction for insurance fraud leaves a permanent mark on an individual’s criminal record, which can have far-reaching implications for their personal and professional life.

- Employment Challenges: A criminal record can significantly hinder employment opportunities, as many employers are hesitant to hire individuals with a history of fraudulent behavior. This can lead to long-term unemployment or underemployment, severely impacting the perpetrator’s earning potential and career development.

- Loss of Professional Licenses: Professionals convicted of insurance fraud, such as doctors, lawyers, or insurance agents, may face disciplinary action from licensing boards, including suspension or revocation of their professional licenses. This can effectively end their careers in their chosen fields.

- Social Stigma: Individuals convicted of insurance fraud often experience social stigma and damaged personal relationships. The breach of trust can lead to isolation and difficulties in forming new relationships, both personally and professionally.

- Financial Instability: The financial repercussions of legal fees, fines, and restitution, combined with potential unemployment, can lead to significant financial instability for perpetrators and their families. This may include bankruptcy, loss of property, or inability to meet financial obligations.

- Insurance Implications: Conviction for insurance fraud can make it difficult or even impossible for individuals to obtain future insurance coverage, or result in significantly higher premiums, further compounding their financial challenges.

The legal and personal consequences of committing insurance fraud are designed to punish and deter fraudulent behavior, highlighting the importance of honesty and integrity in dealings with insurance companies.

For those considering or involved in insurance fraud, the potential repercussions should serve as a strong deterrent, underscoring that the risks far outweigh any perceived benefits.

Insurance Fraud Prevention and Awareness

Prevention and awareness are critical components in the fight against insurance fraud. By focusing on these areas, the insurance industry, regulatory bodies, and consumers can work together to reduce the prevalence of fraudulent activities.

Effective prevention strategies can save billions of dollars annually, maintain fair premium rates for policyholders, and uphold the integrity of the insurance system. Here’s how prevention and awareness efforts are being implemented:

Educating Consumers and Employees

- Consumer Education: Raising awareness among policyholders about the various forms of insurance fraud and their consequences is essential. Insurance companies and regulatory agencies often conduct public awareness campaigns to inform consumers about how to recognize signs of fraud, the importance of reporting suspicious activities, and the impact of fraud on insurance premiums and coverage availability.

- Employee Training: Insurance companies invest in training their employees to detect signs of potential fraud. This includes underwriters, claims adjusters, and customer service representatives who are on the frontline of insurance transactions.

Training programs focus on identifying red flags, understanding the latest fraud schemes, and using data analytics tools effectively.

Strengthening Legal Frameworks and Enforcement

Governments and regulatory bodies play a crucial role in preventing insurance fraud by establishing strong legal frameworks and ensuring rigorous enforcement. This includes:

- Tougher Penalties: Implementing stringent penalties for those convicted of insurance fraud serves as a deterrent to potential fraudsters. Penalties can include fines, restitution, and imprisonment.

- Regulatory Oversight: Regulatory agencies monitor insurance companies and professionals to ensure compliance with laws and standards designed to prevent fraud. This includes auditing practices and investigating complaints.

- Collaboration with Law Enforcement: Insurance companies often work closely with law enforcement agencies to investigate and prosecute fraud cases. Sharing information and resources can enhance the effectiveness of these efforts.

Encouraging Reporting of Suspected Fraud

Advanced technologies, including artificial intelligence (AI), machine learning, and predictive analytics, are increasingly being used to identify and prevent fraudulent activities. These technologies can analyze vast amounts of data to detect patterns and anomalies that may indicate fraudulent behavior.

Insurance companies are also utilizing blockchain technology to create tamper-proof records of transactions, making it more difficult for fraudsters to falsify claims or documents.

Leveraging Technology for Fraud Detection

Creating easy and accessible channels for reporting suspected fraud is essential for early detection and prevention. Many insurance companies have dedicated fraud hotlines, email addresses, or online forms where employees, policyholders, and the public can report suspicious activities anonymously. Encouraging a culture of reporting can significantly aid in uncovering and addressing fraud.

Implementing Anti-Fraud Policies and Procedures

Insurance companies are implementing comprehensive anti-fraud policies and procedures as part of their risk management strategies. This includes:

- Thorough Verification Processes: Implementing rigorous verification processes for claims and applications to ensure the authenticity of the information provided.

- Regular Audits: Conducting regular audits of claims and policies to detect inconsistencies or irregularities that may indicate fraud.

- Fraud Risk Assessments: Periodically assessing the company’s exposure to various types of fraud and adjusting policies and procedures accordingly.

Building Public-Private Partnerships

Collaboration between the public and private sectors can enhance efforts to combat insurance fraud. This includes partnerships between insurance companies, regulatory agencies, law enforcement, and other stakeholders to share information, best practices, and strategies for fraud prevention.

Prevention and awareness are vital to reducing the incidence of insurance fraud. Through education, technology, legal measures, and collaborative efforts, the insurance industry can protect itself and its customers from the financial and social consequences of fraudulent activities.

Investigating insurance fraud is a meticulous process that requires a combination of detective work, forensic analysis, and legal expertise. Insurance companies, along with specialized fraud investigation units and, in some cases, law enforcement agencies, follow a structured approach to uncovering fraudulent activities. Here’s a step-by-step guide on how to investigate insurance fraud:

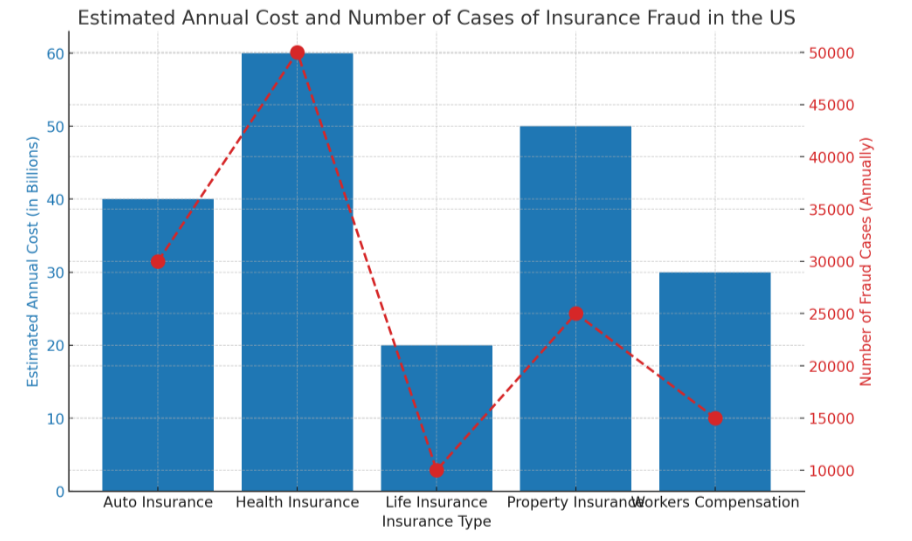

General Statistics and Facts on Insurance Fraud

- Cost to the Economy: Insurance fraud (excluding health insurance) costs more than $40 billion per year, according to estimates from the FBI. This translates to between $400 and $700 per year in increased premiums for the average U.S. family.

- Health Insurance Fraud: The National Health Care Anti-Fraud Association (NHCAA) estimates that health care fraud costs the nation about tens of billions of dollars each year, though some estimates from other sources go as high as $100 billion annually.

- Auto Insurance Fraud: Auto insurance fraud accounts for a significant portion of all insurance fraud. The Insurance Information Institute (III) has noted that fraudulent auto insurance claims vary from exaggerated claims to completely staged accidents. The NICB also reports that questionable claims related to vehicle accidents are a significant component of their investigations.

- Property and Casualty (P&C) Insurance Fraud: The Coalition Against Insurance Fraud estimates that about 10% of property-casualty insurance losses and loss adjustment expenses each year are attributable to fraud.

- Workers’ Compensation Fraud: This type of fraud is estimated to cost businesses billions of dollars annually. The exact figures can vary widely, but the National Insurance Crime Bureau monitors workers’ compensation fraud closely due to its impact on businesses and the economy.

- Life Insurance Fraud: While less common than other types of insurance fraud, life insurance fraud still presents significant challenges, including falsified death claims and exaggerated medical histories. The exact cost is harder to quantify but includes both monetary losses and increased premiums for policyholders.

- Insurance Fraud Arrests and Convictions: Data on arrests and convictions for insurance fraud vary by state and type of fraud. The Coalition Against Insurance Fraud and state insurance fraud bureaus publish annual reports detailing enforcement activities.

- Public Perception: Surveys conducted by organizations like the Coalition Against Insurance Fraud reveal that a significant portion of Americans view insurance fraud as a serious crime, yet a small percentage may still consider engaging in minor forms of fraud, viewing it as a way to “get back” at insurance companies.

How to investigate insurance fraud

Investigating insurance fraud is a meticulous process that requires a combination of detective work, forensic analysis, and legal expertise. Insurance companies, along with specialized fraud investigation units and, in some cases, law enforcement agencies, follow a structured approach to uncovering fraudulent activities. Here’s a step-by-step guide on how to investigate insurance fraud:

1. Identification and Initial Screening

- Flagging Suspicious Claims: The investigation process often begins with the identification of red flags or anomalies in claims or applications. This could be through automated detection systems using AI and data analytics, or through manual identification by trained staff.

- Preliminary Review: Once a claim is flagged, a preliminary review is conducted to assess the validity of the suspicion. This involves a basic check of the claim details, policyholder history, and any immediate inconsistencies.

2. Detailed Investigation

- Assignment to Investigators: If the preliminary review strengthens the suspicion of fraud, the case is assigned to specialized investigators. These individuals have expertise in fraud detection and are trained to handle sensitive investigations.

- Gathering Evidence: Investigators collect evidence related to the claim, which may include documents, photographs, and witness statements. This phase may involve visiting the site of the claimed incident, obtaining police reports, and reviewing medical records or repair estimates.

- Interviews: Interviews are conducted with the claimant, witnesses, and any other relevant parties. These interviews aim to gather more information about the incident and assess the consistency and credibility of the information provided.

- Data Analysis: Investigators analyze data related to the claim, including comparing the claim details against patterns known to be indicative of fraudulent activity. This can also involve checking the claimant’s history for previous claims and looking for patterns of behavior.

3. Forensic Analysis

Expert Consultation: In complex cases, forensic experts may be consulted. This includes forensic accountants, medical experts, or engineers who can provide specialized insights into the claim’s authenticity.

Digital Forensics: For cases involving digital documents or evidence, digital forensic techniques are used to validate the authenticity of electronic records and detect any tampering or fabrication.

Conclusion

Regulatory Compliance: Investigators ensure that the investigation complies with legal and regulatory requirements, respecting the claimant’s rights and privacy.

Consultation with Legal Counsel: If fraud is suspected, legal counsel is consulted to review the evidence and advise on the next steps. This includes determining the viability of pursuing legal action against the fraudster.